#

Research

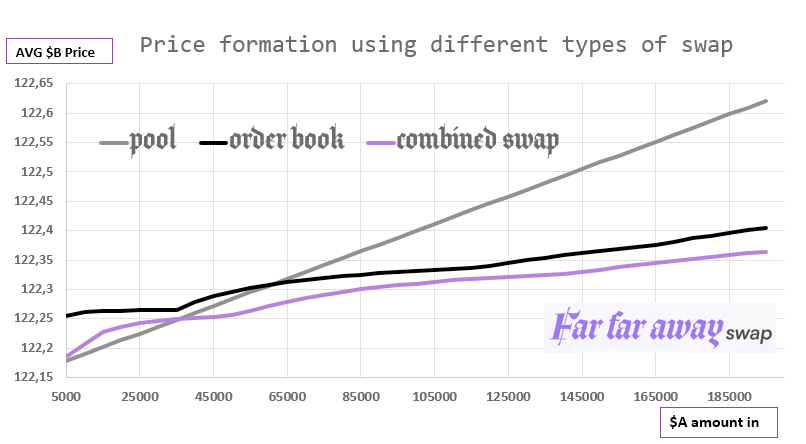

Our goal is providing the best price by using combined swap. To prove the utility of these swaps, we present you our simulations of market price formation when buying in three different ways:

- from pool only

- from order book only

- combined swap

Here is the chart explaining the price formation.

As you see, when we use combined swap, at one moment we reach a better price compared to order book and pool. Now let's talk about algorithms behind these simulations and how they could work in production.

To make this very beautiful

chart we had to simulate the one-moment

abstract market state.

On this market we have the total amount

of $B = N and $A = M and 0.3% transaction fee.

How did we estimate N and M constants?

Easily, this data was downloaded and parsed from Binance,

so once we reach their turnover,

we know how to deal with it.

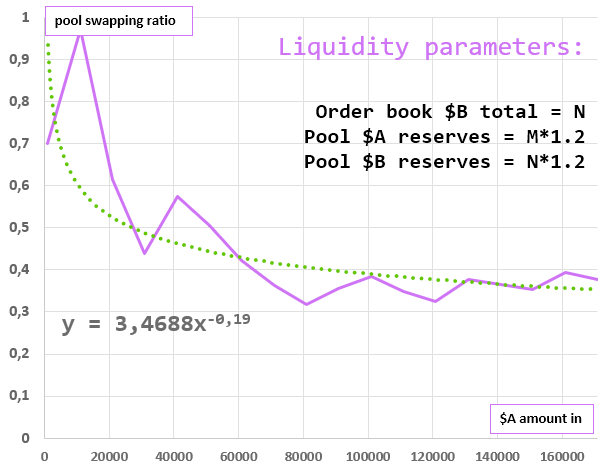

Liquidity parameters in simulations:

- from pool only: we have pool reserves $A=M and $B=N

- from order book only: we use Binance's 98K limit sell orders when in total people sell N $B starting with token price = M/N

- combined swap: we have pool reserves $A=M/2 and $B=N/2, and we use the same order book, but each $B amount is divided by 2

How do our pool works? Exactly the same as on Uniswap V2

For all the simulations we used a very simple python script that iterates trough all possible ratios and chooses the one who gives us the best $B amount out.

def get_optimal_ratio(

amount_inA: float,

orders: list,

step=100,

reserves_in=1254000,

reserves_out=10000) -> list:

"""

calculation of $A ratio sold in pool to get maximum of $B

param orders: test order book data

param step: the precision of algorithm depends on this param

returns: [

<ratio of $A sold in pool to get the max of $B>,

<average $B price>

]

"""

amounts_out = []

steps = numpy.arange(step, amount_inA, step)

for amount_in_pool in steps:

test_orders = orders.copy()

pool_amount_out = get_amount_out_pool(

amount_in_pool, reserves_in, reserves_out

)

ob_amount_out = get_amount_out_ob(

amount_inA - amount_in_pool, test_orders

)

amounts_out.append(pool_amount_out + ob_amount_out)

max_amount_out = max(amounts_out)

max_profit_a_pool = list(steps)[amounts_out.index(max_amount_out)]

max_profit_a_pool_ratio = max_profit_a_pool/amount_inA

token_b_price = amount_inA/max_amount_out

return [max_profit_a_pool_ratio, token_b_price]You can see that this algorithm is not efficient at all O(n) complexity and too much memory usage. However, in production we can avoid using it. How?

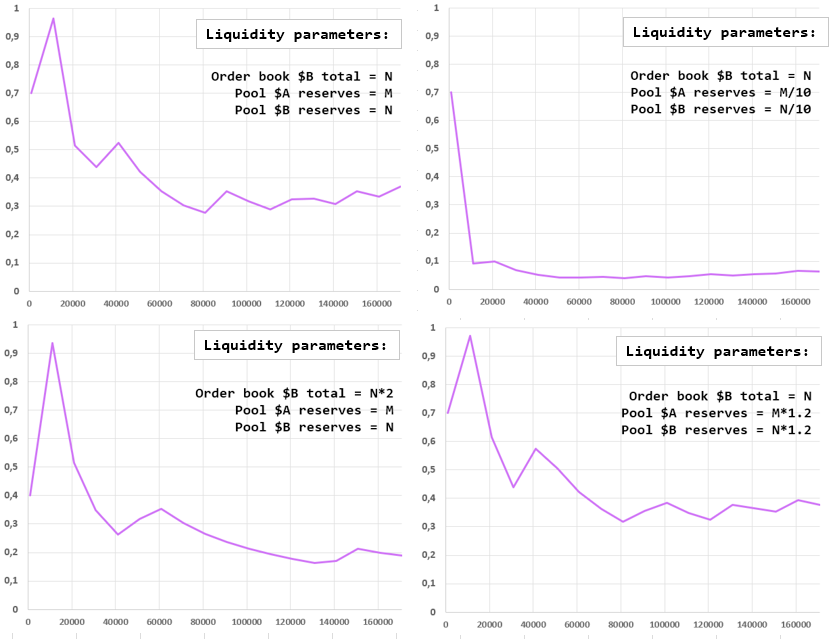

Depending on reserves in pool and order book data, the best ratio curve can take these forms.

- X-axis: total $A we are swapping.

- Y-axis: percentage of $B we buy from pool

As you can see, starting from 10'000 $A swapping, these charts all look like y = k/x^n. This allows us to say that depending on liquidity in pool and order book, we will be able to predict the percentage of tokens we swap in pool due to mathematical model. In this case pool ratio calculation will have O(1)complexity.

As you could see previously, on all the ratio/swap amount curves we can apply a power trendline y = k/x^n like here: